In Framework for Equity Valuation Part II I laid out this approach.

Breakdown of the Equity Price

Using some very simple algebra, I split the equity price into components:

Price = (Price/ Earnings) * Earnings

Price = (Price/ Earnings) * ( Earnings / Nominal GDP) * Nominal GDP

In this work, there was an assumption that the components are independent. I will now examine if this is sensible.

Are P/E and E/GDP independent?

I can find no consistent relationship between the two.

There appears to be a mild negative correlation overall, but at times there can be extended periods of both components falling, such as 1967-74 and 2000-2003, or both rising such as 1994-2000.

An intuitive relationship occurs when there is an expectation of a large rise or fall in earnings and the equity price rises or falls in anticipation. This means the PE ratio would rise in anticipation of earnings rising, and then fall back down as earnings expectations are realised. In this situation, I see earnings as the driver and the PE ratio as a passive variable.

A situation where PE was the independent driver was in the 1980s, when a broad fall in yields meant the PE ratio rose without any need for an expectation of a change in earnings. This supports the approach that we can look at the two factors as independent drivers.

Are Growth and PE ratio related?

This is a relationship that is often assumed to exist as we think periods of low growth or recession are associated with low confidence and high awareness of risk. This high “risk premium” means low PE ratio.

But the evidence to support this idea is not so clear. Of the past 9 recessions, the PE ratio only fell twice. There is some evidence to support the idea that the PE ratio falls in the year before the recession in anticipation of an earnings drop, then recovers quickly as those expectations are realised. This happened in 5 of the last 9 recessions so it is still a fairly mild effect.

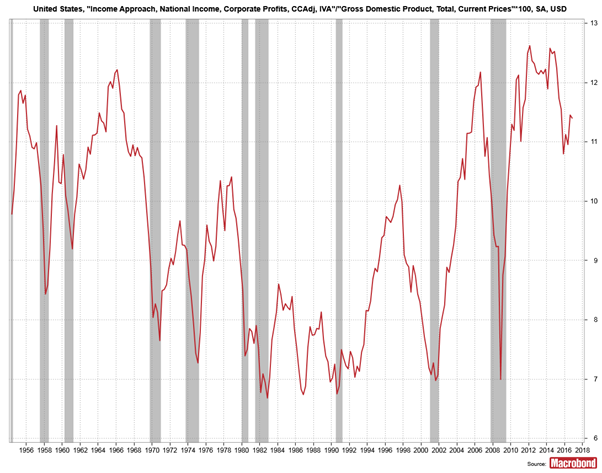

Are Growth and earnings related?

I find the chart below intuitive and compelling. The reason that recessions drive equity markets down is because recessions drive corporate earnings down. If we look at earnings as a share of GDP from 1 year before the recession to the low during the recession they fell each time. The average fall was 21% with the smallest still a 9% fall and the largest (2008) down a massive 42%.

The rationale for this comes from thinking about the breakdown of national income in the NIPA data (Framework for Equity Valuation Part III Earnings Outlook). If there is downward pressure on nominal GDP whilst wages remain sticky, then the impact is felt in a magnified way in corporate earnings.

The magnitude of changes in earnings are very large during recessions and early recovery, so it is during these periods we should be especially alert when forming an equity outlook. The impact of whether growth is 2.5% or 2.8% is imperceptible by comparison. Lots of work by economists, strategists and asset managers is done to fine tune these types of economic forecast but a) it is not possible for them to be that accurate b) even if you could, the relationship to market prices is so loose as to make it useless information.

Conclusion

There is one important interrelationship we need to be very aware of. In previous recessions, earnings as a share of GDP have fallen rapidly and normally bottomed at around 7%. If that were repeated in the next recession, earnings would need to fall by 40% from current levels.