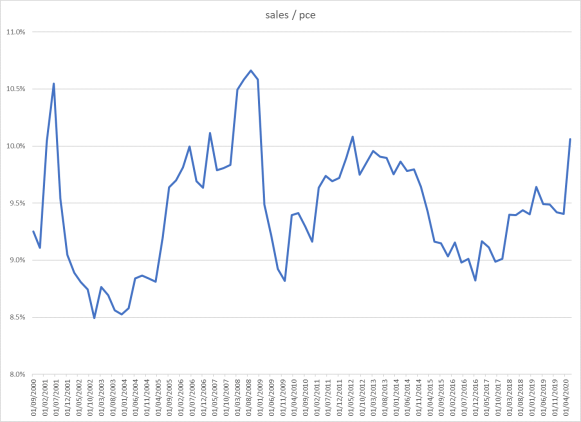

The first thing is to look at the relationship between corporate revenues and the broader economy and to see if it has altered over time. In the following chart, I look at the ratio of:

- Aggregated sales for the S&P 500 (Sales)

- Personal Consumption Expenditure (PCE) from the GDP data

The relationship has not changed in the past 20 years. Revenues of US companies look tied to the spending of the US consumer in exactly the way we would expect. Further, this relationship is why we can look to the performance of the broader economy to predict the overall financial performance of companies.

How about profits/earnings?

The next step is to look at the relationship between corporate sales and corporate profits or earnings. This becomes far murkier, mainly relating to deciding which data you trust on what corporate earnings actually are.

The first issue is to choose which of the many earnings that companies report to use.

Generally Accepted Accounting Principles (GAAP) are a uniform set of accounting and reporting standards to which US companies are required to produce accounts complying to.

You may imagine these would be the earnings that people refer to when calculating the PE ratio (price/earnings) for example, but strangely instead the most commonly talked about earnings are where they “correct” the GAAP for temporary “non-recurring” items. Funnily enough this measure, normally called operating earnings (Op earnings) is always higher than GAAP, with this difference growing to over $20 i.e. over 15% of reported earnings. Here I chart the difference:

GAAP would be clearly a better number to use, as it reduces the discretion allowed to companies to massage their numbers to make them look better to investors. The chart above strongly suggests that at least some of the recent exuberance in the growth of profits is pure cheerleading and manipulation of earnings data. I will further strengthen this argument below.

How do corporate profits relate to the real economy?

The big story of the rising stock market of the past few years has been rising earnings, amid a large rise in the profitability is US companies. Here I look at GAAP earnings versus the Sales series from the first chart.

If we ignore the recessions which play havoc with profits, during the previous good years of 2003-2007 profits averaged around 8% of sales. This was also true from 2010 to 2016. But in the past 3 years we have seen a rise to record levels of profitability. Here I’m even using GAAP earnings which are far lower and more conservative than the operating earnings companies prefer to talk about.

Did this really happen?

There is another way to measure corporate profits which is via the National Income and Product Accounts (NIPA) data, which is the data used in compiliing GDP and looks at the numbers reported by companies in their tax filings. GAAP data has the advantage in that we have it for each company, whilst NIPA data is only reported for the US economy as a whole. The advantage of NIPA data is that it provides much even less discretion to the companies in how they calculate it and so is far less susceptible to manipulation or “optimisation”.

If we redo the previous chart and instead look at the NIPA measure of profits against sales, then the picture of the past decade tells a very different story.

We can see that in good times, profits are in a tight range against sales which makes sense. In recessions (2001 & 2008) profits nearly halved before recovering again. Currently we are observing a drop in profits, which is the usual behaviour before a recession, the opposite to the previous chart which showed an acceleration in GAAP earnings versus sales. The following chart shows it even more clearly.

My real concern with this story of rising corporate profitability is that earnings data reported by companies seems out of line with not only sales but also NIPA data, both of which seem to have much less flexibility in reporting compared to GAAP.

Has this ever happened before?

Yes but it’s a more recent phenomenon. NIPA and GAAP earnings up until the mid-80s had a correlation of 0.9. Since then as GAAP rules have changed, they diverged in the same way in the previous two economic cycles.

The chart above shows a profit cycle which is broadly the same as the economic cycle. In white NIPA profitsover PCE (our GDP proxy as before), in yellow GAAP earnings over PCE.

Profits rise in boom times and do extremely poorly in recessions. The striking difference is that the NIPA earnings are a leading indicator of economic recessions, and GAAP earnings are a lagging indicator. This means clear divergence in the 2 measures cycle peaks, the circles drawn.

In the first green circle, we can see NIPA profits peaking in 1997 whilst GAAP earnings continued to rise until 2000. This was the dot com bubble and we discovered that the euphoria built upon ever rising profits believed to be due to the tech revolution was fundamentally misplaced.

In the second green circle, we see the same thing happening before the Financial crisis. NIPA profits peaked in 2006, but the wonderful results posted by financial firms continued well into 2007, before being exposed as completely fabricated.

Note that these profits reported in 2000 and 2007 were not lies. They were in line with GAAP reporting standards. It is just that late in the cycle, firms get quite good at making sure their earnings numbers keep rising. As I mentioned GAAP reporting leaves a lot more discretion than NIPA.

More recently we saw a small earnings recession in 2014/15 in both the NIPA and GAAP numbers. Since 2016, this is where we have seen the divergence, shown in the red circle. The NIPA data shows a typical late cycle deterioration in profit margins. The GAAP data shows a surge to record levels of profitability and the current set of forecasts expect us to reach even greater heights as early as next year.

Have US companies disconnected from the real economy?

It is clear from NIPA data and sales data that corporations are behaving entirely normally late in the cycle amid falling profit margins. It is clear from all the earnings numbers produced by companies themselves that corporations are still exuberant, having an entirely different relationship with the economy with earnings growing far more rapidly than their sales.

Stock market pricing has risen far more rapidly than the broader economy in the past few years. This seems to fully believe these reported earnings which is why it looks so disconnected from the underlying economy.