For macro trading, thinking about how one asset moves versus another is important.

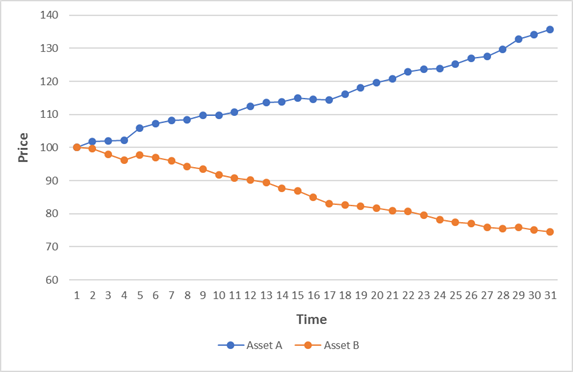

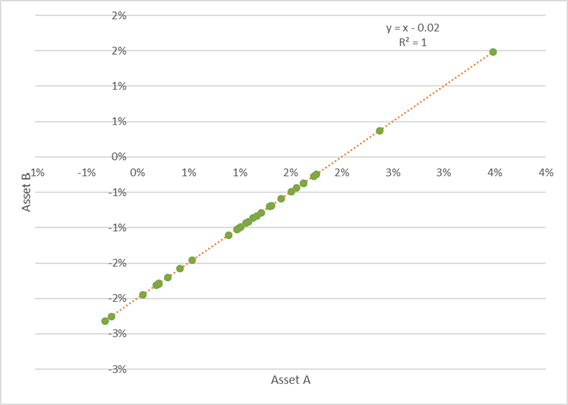

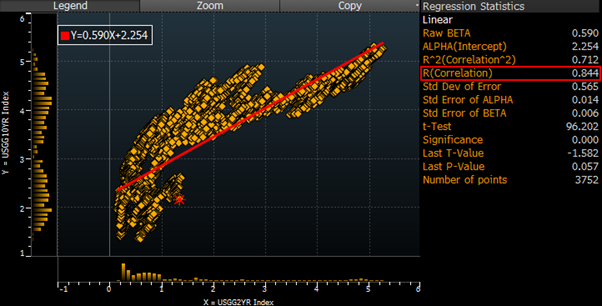

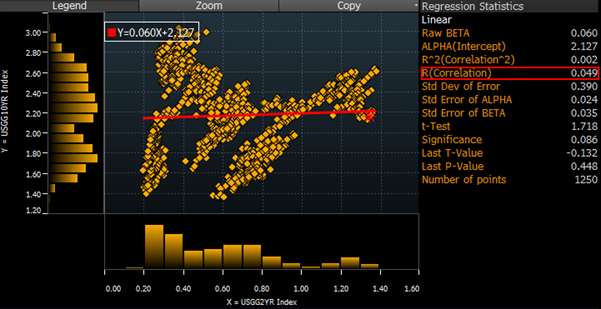

To this end, correlation is most commonly calculated using daily changes. The results of a reasonable relationship might look something like this:

Hedging

This concept is particularly useful if you are a market maker, or anyone in need of a reasonable short-term hedge for your risk. However, if you are holding for a longer period, the potential difference in the trends (the means that we touched on in part 1) are likely to dominate your returns, irrespective of the correlations.

Portfolio Risk

For constructing portfolios, measures like VaR (Value at Risk) are often used to explain and think about risks. The inputs to these measures usually take daily returns.

This can lead to problems with serious consequences if you are using this analysis to understand the risk of a portfolio you are planning to hold for a longer period.

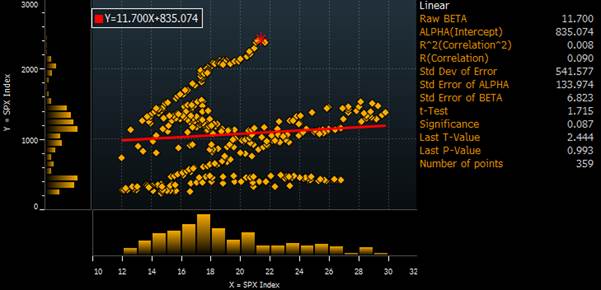

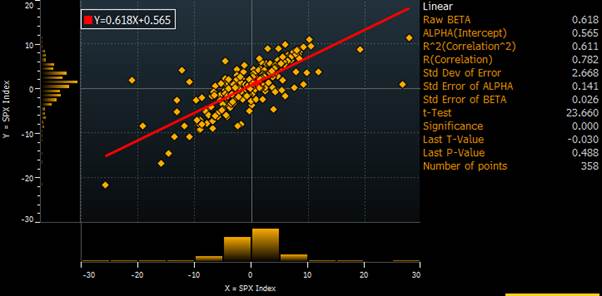

In this chart, I take a selection of major markets that a typical macro portfolio may contain: major currency pairs, interest rates and the S&P.

I plot the correlations of the pairs calculated two ways:

- Return Correlation up the X axis

Taking daily changes as we did previously - Price Correlation up the Y axis

Looks at the correlation of the levels of each price series

(i.e. if both assets went up over the year, implies high positive correlation)

The results are important for the construction of a longer-term macro portfolio. Take 2yr US rates and USDJPY as an example:

- Daily return correlation is decent around 50%

If you are long USDJPY and you add an opposite US Rates position,

Overall portfolio reported risk would therefore decrease

If you hold the portfolio for one day it is reasonable to expect that your hedge will act to reduce the volatility of your returns.

- Price correlation is actually negative

As above your reported risk is determined by the daily return correlation and decreases.

But if you took the supposedly offsetting position above, at the end of year If you lost money on USDJPY, you would have lost on your “hedge” too

The “hedge” would have reduced your reported risk but increased your return volatility on a one-year horizon.

So what does a “good hedge” look like?

Two plausible but very different definitions seem clear:

- High correlation of daily changes

Consistent with VaR and best hedge for VAR, short term traders, market makers, options traders (delta hedging). A lot of option hedging is done via proxies and this is the type of statistic they would care about.

- Long term hedge

Much more important for longer term position such as a macro hedge fund, a pension fund or your personal portfolio. There a hedge would mean that if you hold both assets for a year they would have similar (offsetting) P+Ls

The above analysis shows how different these two time horizons can be. The big risk we face as portfolio managers, is that we do too much of the analysis based on short term price changes, which links conveniently to VAR style risk reporting. This gives a completely misleading guide on the long term P+L risk we are actually taking.

Conclusion

In these pieces, we have seen that Correlation is probably not what you thought it was.

Correlations are used in risk reporting (as we have mentioned here) but also in Portfolio Theory, CAPM and how an investor should think of designing a portfolio.

This topic has important ramifications for many areas of modern finance and I will return to it later.

and

and  are critically important but this importance is rarely appreciated. [1]

are critically important but this importance is rarely appreciated. [1]