You can also find this link on the home page of this blog by clicking the ‘Substack’ button in the top right

I will be posting new material on substack and will no longer be posting on this blog.

Below is a copy of my new post, the introduction to a new series exploring whether we are currently in a stock market bubble. The follow-up pieces can be found on substack.

The 2026 Stock Market Bubble

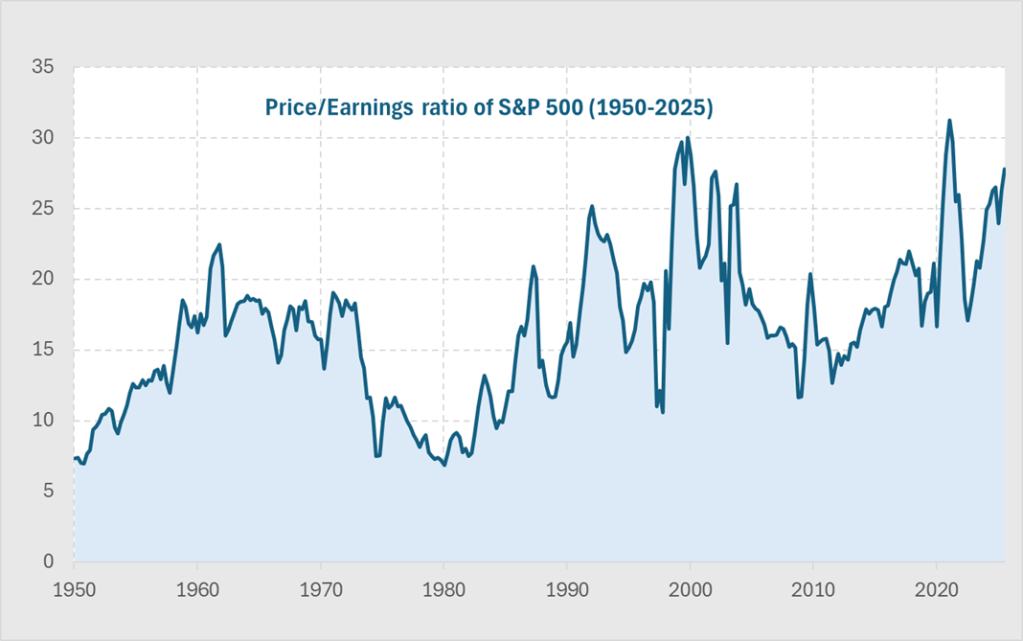

The US stock market sits at levels that look extreme by any historical comparison. These extraordinary times require a more rigorous analysis than just high Price-Earnings (PE) ratios or anecdotes about AI company valuations.

If you have investments, such as a pension, 401(k) or an ISA, you need to make decisions about how you allocate your assets. Whether or not OpenAI is worth $840bn is not relevant to you, it is a private company. What matters to you is whether the broad public market is cheap, fair value or expensive.

Today’s elevated PE ratio in the S&P generates a lot of press attention, but it simply reflects strong optimism about future earnings. That alone cannot tell us whether we’re in a bubble like dot-com in 2000 or on the early stage of AI driven earnings revolution.

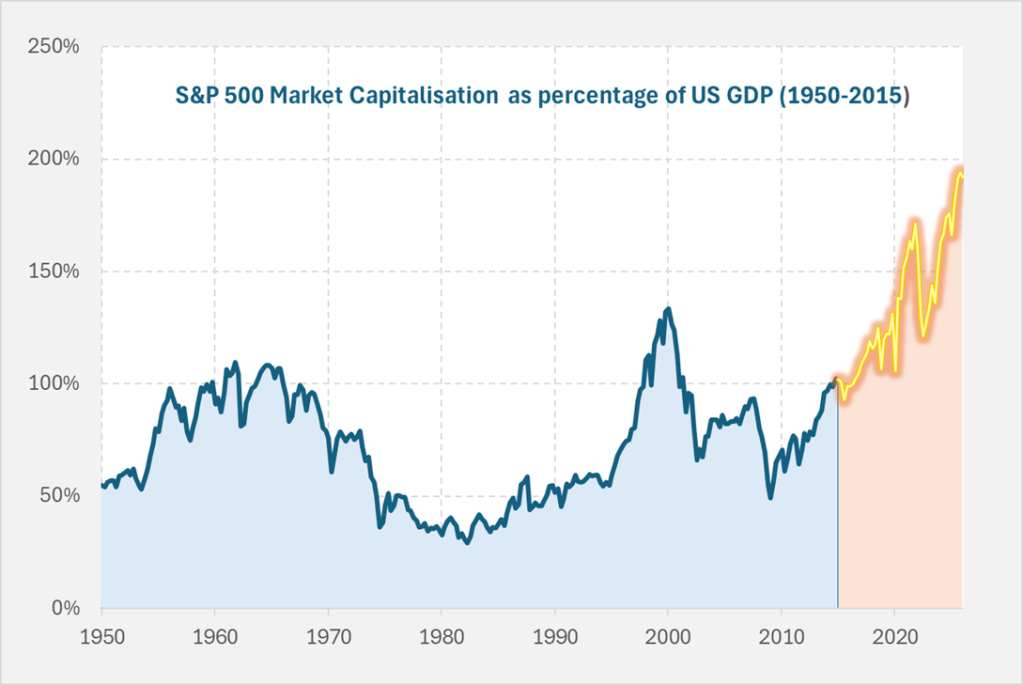

The US stock market has become enormous relative to the size of the economy. Below we show the value of US equities as a share of overall GDP. It is double what it was a decade ago, and far higher than we saw in the dot-com bubble of 2000.

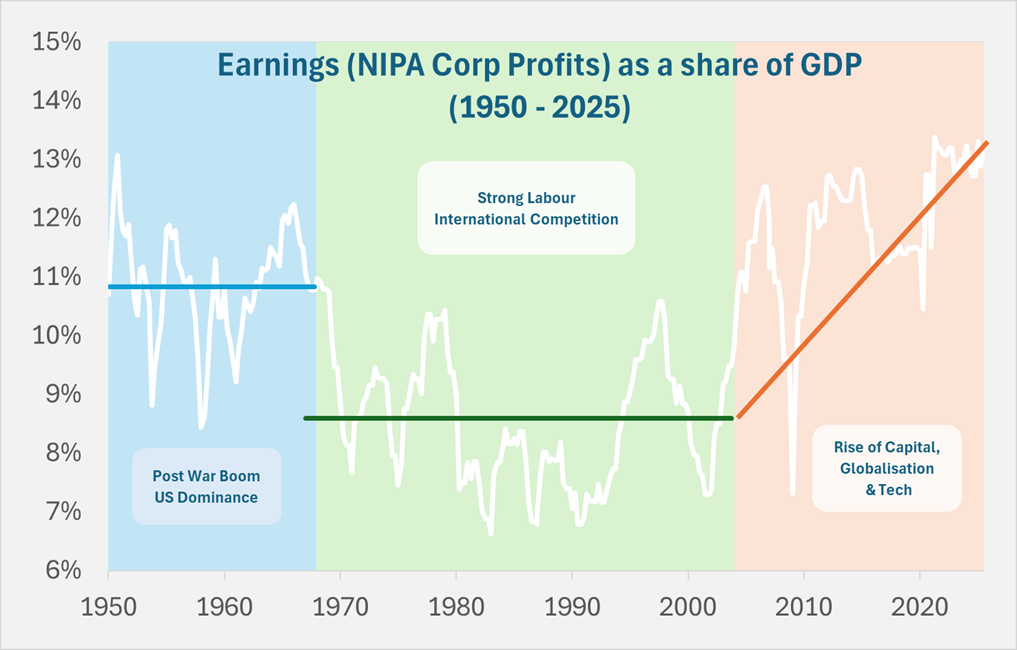

The reason this chart looks more extreme than the simple PE chart is that underlying earnings as a share of GDP has already reached unprecedented levels over the past twenty years. This rise in corporate profits from around 8.5% to 13% of GDP has seen wages stagnate, widening economic inequality, and a political backdrop marked by discontent and populist movements such as MAGA.

Current valuations show the same level of optimism about future earnings growth as in 2000 dot-com bubble, except today’s level of earnings are far higher. It is this combination that is so extreme.

What would this earnings share need to be over the next decade for your stock market investment to simply keep pace with GDP growth? The chart below shows

The projections are stark.

Current valuations assume future jumps in profitability that dwarf anything ever seen. Can AI really deliver a surge in corporate profits far beyond the gains achieved in the last waves of globalisation or past technological booms?

This series will continue on substack and examines the extraordinary claims behind these extraordinary times.

I am confused by the calm coverage of the recent radical shift in economic policy – described by the BBC as “bid to boost growth”. This type of reporting does not make clear whether we are talking short-term growth or long-term potential, and how these policies impact each of them in very different ways. From conversations with friends, much of the analysis does not investigate this and ultimately reveal just how dangerous and radical this new set of policies is.

Potential Output – what is it?

Truss has justified her policy changes economically citing improvements in the UK’s long-term growth potential i.e. increasing potential output

Potential output is the starting point for thinking about how much the country can produce ie it is the maximum sustainable level of output.

If we are below, then this is called a negative output gap and we see things like unemployment rates being high and inflation likely falling.

The OBR does a great job on this and their website is very clear

Potential Output – how can we improve it?

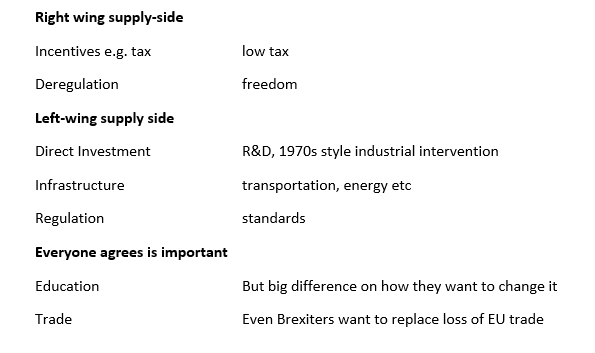

Everyone wants to improve potential output and there is a clear left vs right divide on how best to achieve it.

Truss is firmly in the right-wing supply-side movement of “trickle-down” i.e. give tax breaks to rich people and everyone will be better off because somehow this leads to greater potential output. Reagan was the most prominent exponent of this view but we are still waiting for any evidence that it works.

Potential Output – will it work?

I think best to simply summarise that there is no evidence that cutting taxes has any positive effect on potential output. OK – so if Trussonomics does not improve potential output, what does it do?

It does a LOT

The most obvious and direct impact is of course on inequality. She is delivering a massive cash handout to rich people. The richer you are the more you get.

The part that is getting less attention is the impact on

Fiscal vs interest rate policy mix

Debt sustainability

Fiscal vs interest rate policy mix

This policy choice has been perhaps at the heart of the political battle of the past decades and is commonly misunderstood. This is a shame as a simple quadrant model does a good job of providing a framework to compare the options clearly. (Fiscal policy is the mix of tax and spending with high spending/low tax being loose fiscal policy)

Tight fiscal -tight monetary When you are committed to fighting inflation above other policy goals. For example, the 1980s or commonly after an economic crisis when trying to rebuild confidence in the currency and debt. If used inappropriately looking at the 1930s Great Depression.

Tight fiscal – loose monetary This is the Cameron years. There is of course a debate over how tight fiscal policy should have been and on how the mix of tax and spending was managed. But it is a consistent policy mix

Loose fiscal – loose monetary This was at its maximum during the pandemic i.e. for a short term huge negative shock. If used long term it just leads to economic catastrophe.

Where are we now?

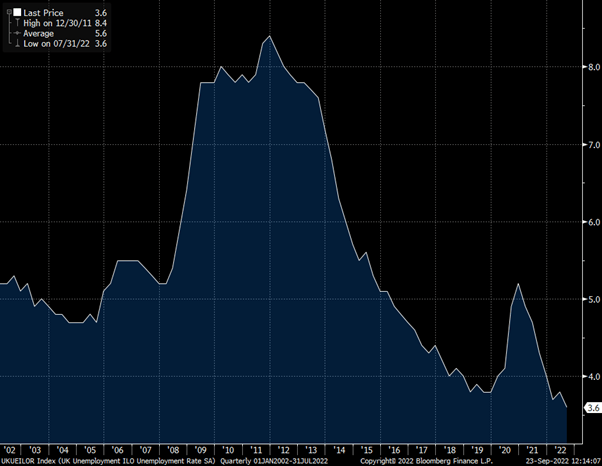

We are currently in the loose/loose box. Taking the unemployment rate as a simple measure of the output gap, you can see from the chart below we are at record lows. This is also clear to anyone trying to hire at the moment and all the reports of staff shortages. Which makes it odd that Truss talks about “boosting growth” as there is no prospect of lower unemployment from here.

UK Unemployment at record lows

The other factor that makes going for growth an odd policy goal is that inflation is high and rising. This does not have an easy solution and economic pain is unavoidable. Trying to avoid it, leads to even greater pain later.

UK Inflation at 30-year highs

What happens next?

The Bank of England will be forced to raise interest rates by huge amounts. At the start of this year the market expected interest rates to stay at around 1% though 2022 and 2023. Now the market expects rates to be 4% by the end of this year and 5.5% by the end of next year- with rate expectations for next year shifting 3% since the start of August.

What does this mean for people?

Well rich people have had a large tax cut and will be fine – I know you are all relieved to hear this.

Anyone on a regular income has had a small tax cut but this will be dwarfed by the rise in the mortgage payments coming soon.

What does it mean for the economy?

I predict a very bumpy path and hard landing for the economy but difficult to say when. The policy mix of vast fiscal expansion at a time of low unemployment and high inflation to be offset by rapid interest rate rises is a chaotic mix. I think the economy will stay strong and then crash hard.

Debt sustainability

This is getting some attention but is being dismissed by Truss. The fact that they did not let the OBR produce a forecast tells us a lot about how they have contempt for this constraint on policy. An Office of Budget Responsibility is not what the Chancellor wants to hear from!

But the bond market still exists, and long-term government borrowing is getting hammered. 30-year Gilt yields have risen from under 1% at the start of the year to 4% as I write this.

The tax cuts and extra spending increases the budget deficit. The rise in interest rates increased the cost of servicing the debt, further increasing the budget deficit. This can become an exponentially explosive mix with the major accelerator being a currency crisis as the value of sterling falls.

Conclusion

The Trussonomics experiment is radical and dangerous. I expect high inflation, high interest rates and a weak currency leading to economic crisis. Politically I expect her to start to blame the Bank of England as though the rise in interest rates was not a direct result of her policies. The Bank of England may be independent of the government, but they are not independent of economic reality.

Truss has spoken of her disdain for “abacus economics” and she does not believe things need to add up. I think economic reality exists and her magical money tree fantasy will fail.

As the rollout of COVID vaccination programs progress, the issue of reaching as many people as possible becomes critically important.

The anti-vax movement gets a lot of press in the news but that is not the group I want to talk about. They seem to be broadly typical of conspiracy theorists, so there is nothing I have to say which would make any sense to them.

The group that is far more interesting are the vaccine hesitant, who are not conspiracy theorists but often have rational foundations for not wanting to take the vaccine. I should be clear that I am very pro-vaccine and got mine as soon as I could and encourage others to do so, but I would like to explain why and how my views might differ to a vaccine hesitant person.

My friends and family don’t trust it so nor do I

I would think this is the most common reason and the most easily understood. They will often put more weight on the opinions and behaviors of those close to them, and so it should not be a surprise that vaccine enthusiasm/hesitancy exists in pockets with groups of friends and family likely to have similar views. Reaching out to communities in ways that make sense to them is key and there is no simple answer.

I have a personal history to not trust new medicines

This is very real and very understandable. People who have had bad experiences with other medical treatments are likely to be cautious and require more convincing to participate.

I don’t trust the government

Nor do I. I have a lot of sympathy with people who are confused by the messaging and have lost faith in this government. Boris and his cronies lie all the time; they have used the crisis to create a kleptocracy where they and their friends are given lucrative contracts and serial failures like Dido Harding are promoted and given £37bn to waste. I am particularly annoyed that in the chaos of Boris Johnson’s government, important public health messages are often hidden.

But thankfully we do not have to take Boris’ word for the vaccine being good. The globally available information is compellingly behind the vaccination program including every government, international agency and scientific body. To think that there is collusion between all of these groups takes us into the realm of conspiracy theorist rather than hesitant. A good rule of thumb to know whether a conspiracy theory is plausible is to think about how many people have to be in the conspiracy and for how long. Tens of thousands of unconnected people keeping the massive secret for over a year is just not possible.

I have Information overload

There is vast amount of information available on COVID and the vaccine. Plenty is true but complicated, and a reasonable amount is misinformation. Sorting through it is not simple, especially for a general population with no particular training in medicine, statistics or ethics with low trust in authority.

In the face of this, people can find it very hard to make decisions and ‘doing nothing’ becomes the default and easiest outcome.

The technology is too new

mRNA technology has actually been around for a long time. The first vaccines were developed 30 years ago and 10 years ago we had good working candidates. But it took the pandemic for the funding and regulatory attention to move them into production. https://www.nature.com/articles/d41586-021-00019-w

I expect to hear much more about this technology in the coming years as we develop new ways to treat diseases such as cancer.

The vaccine was rolled out too quickly to be safe

This was a concern of mine but some research last year showed that a lot of the slowness in previous vaccine approvals came from bureaucratic delays rather than safety requirements. Much of the approvals process can be done simultaneously rather than sequentially which really sped things up. Similarly the vast funding enabled us to develop later stages of the research before waiting to finish the early stages.

Also, each vaccine had to be separately approved by each country’s own regulator ie you have a very large number of independent entities with chance to raise issues with the vaccines or the process.

It is best to wait to be sure it is safe

This makes sense as an argument. The reason I do not agree in this case is that normally you would be waiting until lots of people have done it in case there is a problem which the testing stage missed. This normally takes time but given the speed of the rollout this time there have now been 5.6 BILLION doses delivered. This is an unfathomably large number, so far above the number you need to get approval which is in the thousands.

I am worried about the side effects

This would be a sensible reason for hesitation and is a normal human response. I do not share it as, related to the point above, we know so much from those 5.6 BILLION doses. With that many doses, it would be a shock if there were no individual tragedies, but the scale of the rollout means that our confidence is very high that the risks are vanishingly small. Unlike for COVID where the risks are well documented and much higher. For example, the risk of blood clots from the vaccine do exist but are vastly less than the risk of blood clots from COVID.

A complicating factor is misinformation about side-effects (e.g. leads to fertility issues or contaminates breast milk) – these are simply untrue.

Another common fear is that there might be a long-term problem (e.g. you will get cancer in 20 years’ time). I do not have much to counter this except to wonder why no other vaccine has ever had that problem. I am also very well aware of the long-term effects of COVID which are very real and could be very severe so I would much rather be protected from that.

I value my freedom and do not want to be forced to take it

This argument feels backwards as freedom for most people increases if we all have the vaccine as the vulnerable can safely leave their homes. I wonder if they feel this way about other forms of government coercion and want to protest their right to drive through red lights at 100 mph outside schools while drunk. Sometimes society limits our “freedom” to damage other people.

The vaccine does not really work

The argument here is that you can still catch COVID after being vaccinated. This is true but misses that you are drastically reducing the risks of more serious problems and virtually eliminating the risk of death.

Similar arguments are made about masks and other prevention measures, but I think this is a conceptual error on safety. Reducing risk is still a good idea even if it cannot be reduced to zero. I happily wear a seat belt and drive a car with an airbag even though it is still possible to die in a car accident.

The best metaphor I have seen about combining risk reducing strategies is to think of each of them as a slice of Swiss cheese.

Any single slice has large holes in it. But put them all back-to-back and you cannot see through it.

Some of the slices such as masks may have larger holes and some like vaccination have smaller holes. They are not alternatives but work best in combination.

You can still pass on COVID if you are vaccinated and so my decision only affects my health which is my business

This has some appeal as an argument. Even if you are double jabbed then you can still catch COVID and you can still infect other people. So what is the point?

This is misleading because vaccinated people:

are less likely to catch COVID ie less likely to have it

likely to have a much lower viral load ie are less infectious

are likely to recover much more quickly ie are infectious for less time

The combination of these three means that you do not have the exponential growth in the population and the virus dies out.

Conclusion

With a little reflection, it is pretty obvious that if no one were vaccinated right now, deaths in the UK would again be in the thousands per day not dozens. If everyone took the decision to delay, we would collectively be in a terrible situation.

In fact, a notable positive from the rollout has been how large the take up has been. Polls suggested that a large number would not take the vaccine but the take up has been far in excess of that.

This suggests to me that the anti-vax believers have likely not changed their mind but the numbers of vaccine hesitant has been steadily reducing. The arguments I have made above are far from new, and people are gradually moving towards accepting the vaccine.