Recently in the news

- You may find it puzzling that Republican voters are still backing Trump.

- You may be amazed that the same voters do not believe that Russia interfered with the election, or that there is any connection to the Trump campaign.

- In that case you must be shocked that the recent Donald Junior revelations have make their belief in ‘no collusion’ even stronger.[1]

But then again, is it that surprising? I previously discussed confirmation bias and desirability bias (https://appliedmacro.com/2017/07/10/decision-making-systematic-flaws-biases/ and https://appliedmacro.com/2017/07/12/desire-the-fatal-flaw/)) but in this case feels like there is a different driver at work.

“Backfire effect”

This recent paper [2] found that “direct factual contradictions can actually strengthen ideologically grounded factual beliefs”. This is the “backfire effect”.

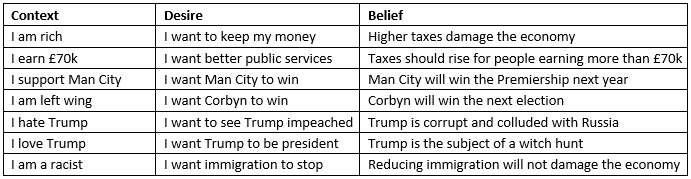

In contrast to what we saw previously:

Here we have:

The more evidence and the clearer the evidence against Trump, the more strongly his supporters believe him innocent. Trump supporters are not backing him because of facts or policies, this is about ideology and culture and it is a battle. Facts are irrelevant.

There are plenty of examples which demonstrate this. Tim Harford talks about how the tobacco industry managed to delay regulation for decades despite overwhelming evidence showing the link between smoking and cancer. [3] Another favourite example is what happens to cult members who believe that the world will end on a specific day. They give away their possessions and prepare for their ascension to heaven/alien spaceship. When the day arrives and nothing actually happens, they do not lose their faith; their faith in the end of the world actually increases. Perhaps the “backfire effect” also explains why Tony Blair’s support for the Iraq War became more fervent despite mounting evidence against the entire premise.

Back to Trump-gate

Given this, I fear that this ever-larger number of smoking guns will not help the Democrats much, even with increasing suggestions of criminal activity not just from the Trump campaign but from the Trump family itself. The way to defeat the Backfire effect is not to counter with ever more evidence. There was no possible evidence based argument that would have changed Blair’s mind about war.

The best approach is to build a compelling alternative narrative. Corbyn did this very successfully in the last election, making no attempt to defend himself against May’s attacks, focusing only on what he wanted to talk about. He did not change people’s minds about Trident, he stopped them thinking about it. What we focus on is far more important than the content of the debate.

Like all cognitive biases, spotting them in others is far easier than in oneself. We can all fall foul of the “backfire effect” when it comes to our most central values and beliefs. For business and investment, it has perhaps led to the most catastrophic of errors. The disasters of RBS, Lehman and Enron can be traced to core beliefs that proved successful at first, but then warning signs were ignored as the management became ever more evangelical in their confidence that their path was the right one.

When we are looking for investment analysis or advice, then we should be very wary of those with high and unchanging conviction. Some of the ones I regularly come across: the EU will break up/stick together or China will implode/ take over global dominance or the bond market will crash/inflation will never return. They argue passionately and eloquently (they are well practised) but are the ones most likely to be victims of the “backfire effect”. The element that makes them so popular as guru strategists and TV pundits makes them highly unreliable sources of investment advice.

Perhaps we should simply recognise that we may easily fall for this as individuals, but by building diverse enough teams and open enough culture, we may not fall for the same cognitive flaws.

Summary

As with confirmation bias and desirability bias, the “backfire effect” is important and can warp your interpretation of the world. Your political enemies and people you do not respect will not be the only victims of this. We can all fall prey to it and should be most sceptical of our views which are most closely linked to our core values and beliefs.