In a previous post, we looked at a model of relative value of equities versus bonds (https://appliedmacro.com/2017/05/09/are-equities-expensive-part-i/).

But it does beg the question of whether bonds are good value themselves.

I am not aiming for a full review of global bond value, I will focus purely on the US market. In this post, I shall look at the front end of the curve and in a later post the long end.

Expectations

The simplest and best model for the short end of the yield curve is the expectations hypothesis.

The yield is an average of short-term interest rates that are expected to prevail through the life of the security

Such expectations may not match the market yield, so there may be a residual. This residual r is sometimes called the premium (choose any: risk premium, term premium, liquidity premium, it does not matter which). At times such as during the financial crisis, I spent a long time modelling precisely the premia, but in normal market conditions it’s not very productive. Merely knowing if the premium is large or small, positive or negative is sufficient.

The other term often used for premium is expected return. If you think in terms of academic “efficient market” models or asset allocation in a real money environment, then you may prefer to use excess return but the language does not matter here.

US Front End

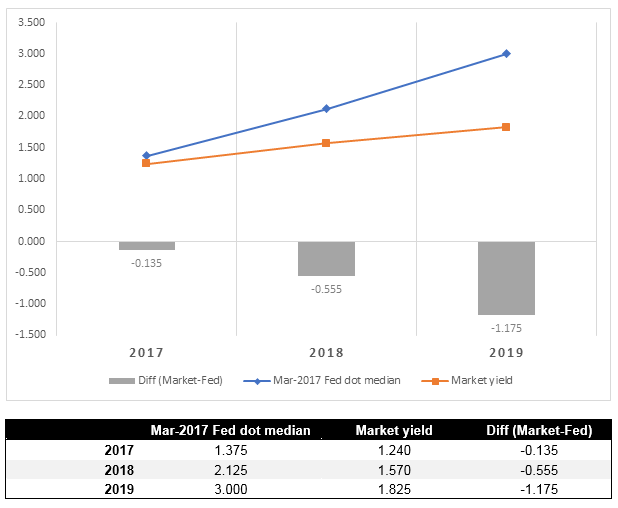

In the US, the Federal Reserve effectively sets short term interest rates, the Fed Funds rate, and these days they helpfully publish quarterly forecasts of where the committee thinks it will be. A sensible starting point is to compare these forecasts to the tradable yield and calculate the residual.

If you have not been following fixed income markets for the last few years or have learnt how markets work from finance textbooks, you may find this chart surprising.

We, as market participants, are well used to the fact that the market is pricing that rates will be significantly lower than the people who set them expect them to be. This has been the case for a long time but so far, the market has been better at predicting how the Fed will behave than the Fed itself.

If we look at a chart over the past 2 years where rates have been expected to be at the end of 2018, we see some fluctuations but very little net movement. In contrast, the Fed has been consistently revising lower its forecasts of where it thinks rates will be.

If we cannot just assume the Fed know what they will do, we must form our own opinion on where rates might go and determine whether the market is under or over pricing the path. The way to do this is to break down the elements of the forecast and analyse each of them.

The Fed’s reaction function & the Taylor rule

To start with the obvious, the Fed decision can be thought of as a function of things they care about. It is often called their “reaction function” and the things they care about are employment and inflation, their explicit objectives as given to them by Congress.

A common and useful form of this is the Taylor rule, which models Fed behaviour on just two variables.

Using this to make investments

The Taylor Rule is not that useful as a predictor of rates, but it forms a useful framework to think of what drives them.

There are 3 obvious places where you can disagree with the market and so make an investment call.

- A different view on growth

One of the largest and most obvious trades in my career was short term rates in 2002. The economy had been very poor in 2001, but the memory of the bubble was perhaps still so vivid that the market priced a rapid rebound in growth and thus interest rates. 2002 did not turn out to be the year of recovery and rate expectations fell accordingly all year.

- A different model of the economy

A good example of this would be 2008. Even after Lehman went under in October 2008, it took a long time for people to understand how serious it was and the devastating impact on the broader economy. The market was still pricing that rates would be nearly 3% at the end of 2009. They ended up close to zero. Rates eventually plummet in 2008 because the economy is falling apart.

A counter-example where a commonly believed idea turns out to be wrong is the idea that Quantitative Easing (QE) is going to lead to high inflation and so bonds will collapse. This comes from the idea that inflation is caused by “money” and the Fed is “printing money”. A simple and appealing argument that comes from a misunderstanding of what “money” is and how the monetary and banking system works. (a good topic and controversial later post I am sure).

- A different view on reaction function.

An example here would be that after the crisis many people were very premature in thinking that the economy would get back to normal.

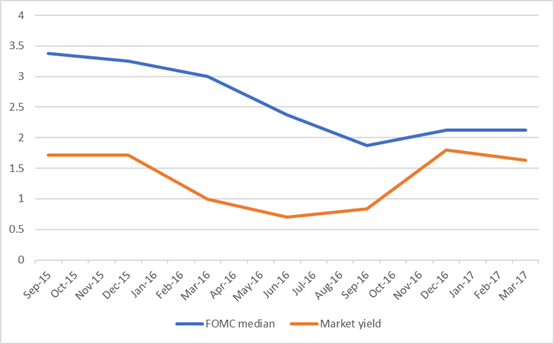

In the summer of 2013, rates were still zero and the Taylor Rule suggested that was appropriate. But taking the economic forecasts at the time and projecting what that meant, suggested that rates would be much higher. So back in 2013 the market was pricing that rates would currently be about 3 %. In fact they are around 1%.

This difference is not because the economic growth forecasts were wrong. But the reaction function was. If you listened to Fed Chair Yellen’s speeches she was clear that the Fed would be very “patient” in raising rates. They desperately wanted to avoid hiking prematurely and actually wanted inflation to be higher. So a new reaction function should have been understood – that the Fed were waiting longer to hike to get the economy to be running hotter.

What about now?

My experience of financial markets is that is that expectations are more commonly adaptive than rational. By this I mean that humans (including market participants) tend to overweight recent experience. Given that the Fed has been consistently too high in their forecasts for the last few years, people expect that will continue to be the case. I am not so sure.

I am inclined to use an even simpler new reaction function for the Fed based upon wages. In previous cycles, they would hike before wages rose because

- They were confident in the economy

- Inflation and wages were high enough already to take a risk if they go lower again

- Wages are a lagging indicator, so by the time wages rise the economy will have been running too hot for too long

This time they want wages and inflation to be higher before they even start. The data suggests to me that wage growth is finally recovering.

It is reasonable to think that the economic cycle works the same now as in previous periods, and so wages are a lagging indicator. That means that the labour market has been tight for a while now and is continuing to get getting tighter adding more upward pressure on wages.

Conclusion

This cycle has been very different from prior periods because

- The recession was very deep

- The recovery was slow

- The Fed wanted to wait until they were sure they needed to raise rates.

This has meant that being long the front end has been a reasonable trade for a long time i.e. the front end was cheap against my expectation of where the Fed would set rates. But with the signal that wages are finally rising, we may be approaching the end of this phase. Furthermore, with so little still priced for rate hikes from the Fed the front end does not look good value to me.

If the US recovery has been slow, but the economy not long-term impaired then this means that the rate cycle has been delayed, not that it is not coming or that where rates end up will be so much lower than in previous cycles. But that is the topic for the next post.

One thought on “Framework for valuing fixed income – Front end”