Introduction

For anyone interested in the long-term investment outlook for fixed income, or more simply the future of our current sovereign nation states, an understanding of government debt must be a key element. Much is written on this subject but I find a lot of it confusing with partisan politics dominating analytical perspectives and terminology which is often inconsistent and emotive.

In this note, I want to focus on episodes where large debt level has been managed.

The large debts of WW1 and the Great Depression were reduced, on the whole, by various types of default. These always come with large economic costs and are to be avoided.

The period after WW2 is more interesting, commonly used as evidence as grounds for optimism and as grounds for opposing “austerity”. (in quotes as this term is generally emotively used by the opponents of current fiscal policy and has a pretty loose definition and usage)

(This paper by Reinhart and Sbrancia does a nice job of laying out the economic history. https://www.imf.org/external/np/seminars/eng/2011/res2/pdf/crbs.pdf)

Government Debt Model

So, I thought I would start by making a simple framework within which I can look at debt dynamics. Breaking down the change in government debt into 2 parts:

- Primary surplus

- Interest payments

(put simply Overall Deficit = Primary deficit + interest paid)

Note, this is not intended to be a complete model as there are clearly other factors which can change the debt level. For example

- Change in currency level for foreign-denominated debt

- Change in yields leading to change in market value of the debt

- Due to Extraordinary items e.g. the government takes on additional debt which for accounting reasons they do not show up in the primary deficit

But it is pretty decent and captures the vast majority of the debt dynamics, certainly all of the ones which drive long-term trends.

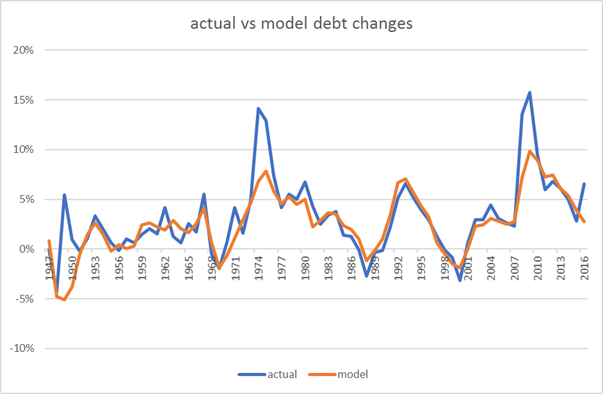

Model UK Gilt History

Here is the model vs actual data since WW2 for the UK.

There are two clear episodes (~1974 and ~2008) when the actual increase in government debt were far larger than the model would suggest. It would be nice to understand what drove it (for example, in the financial crisis, did the government balance sheet absorb private sector banking debt without having it showing up in the deficit?)

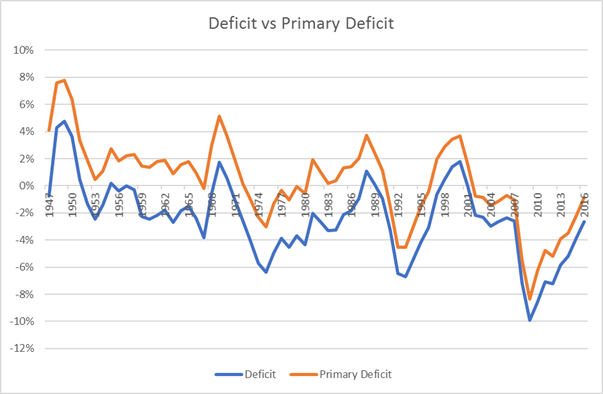

Below is the chart of UK debt since WW2

It is commonly described that the UK ran deficits thought this period and the debt level was brought down by high growth. This is not incorrect but I find it a bit narrow and misleading.

Budget Deficit v Primary Deficit

First, the idea that the UK ran deficits. Well it is true but if you split the deficit into primary surplus/deficit and interest payments then the picture looks quite different.

During the 1950s and 60s, the UK run a deficit virtually every year. But we can also see that the UK ran a primary surplus for the entire period. So the reason the UK ran a deficit was simply that the debt levels were very large and so the interest payments were very large.

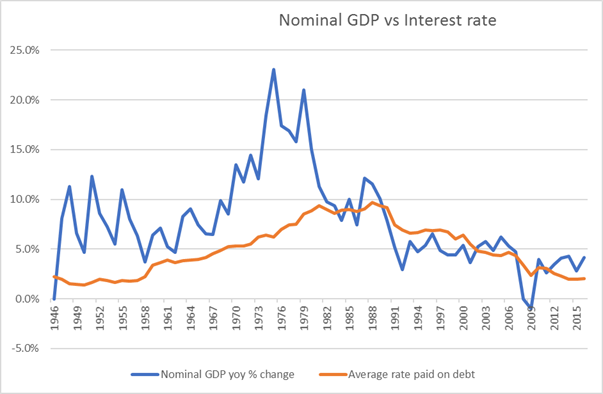

Whilst it is true that the main way the UK brought down its debts level was running nominal GDP at a higher rate than the interest rate paid on its debt, compounding effects are huge (running this for a long time) particularly when the debt level is large.

Between 1947 and 1951, debt levels fell from 246% to 165% of GDP. The cumulative primary surplus over that period was 29%, so the balance, about 2/3, of fall in level came from the impact of nominal GDP vs the rate on the debt. compared with only 1/3 from running large primary surpluses.

Relevance to the present

How did the UK manage to keep its rates so far below nominal GDP?

Should we expect to be able to do the same in the future?