You can also find this link on the home page of this blog by clicking the ‘Substack’ button in the top right

I will be posting new material on substack and will no longer be posting on this blog.

Below is a copy of my new post, the introduction to a new series exploring whether we are currently in a stock market bubble. The follow-up pieces can be found on substack.

The 2026 Stock Market Bubble

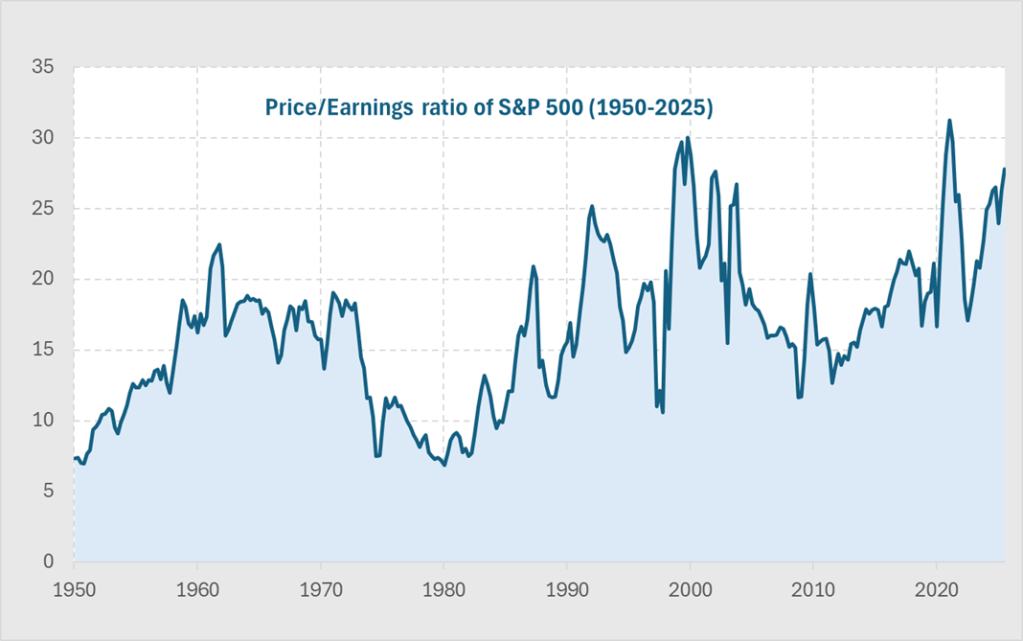

The US stock market sits at levels that look extreme by any historical comparison. These extraordinary times require a more rigorous analysis than just high Price-Earnings (PE) ratios or anecdotes about AI company valuations.

If you have investments, such as a pension, 401(k) or an ISA, you need to make decisions about how you allocate your assets. Whether or not OpenAI is worth $840bn is not relevant to you, it is a private company. What matters to you is whether the broad public market is cheap, fair value or expensive.

Today’s elevated PE ratio in the S&P generates a lot of press attention, but it simply reflects strong optimism about future earnings. That alone cannot tell us whether we’re in a bubble like dot-com in 2000 or on the early stage of AI driven earnings revolution.

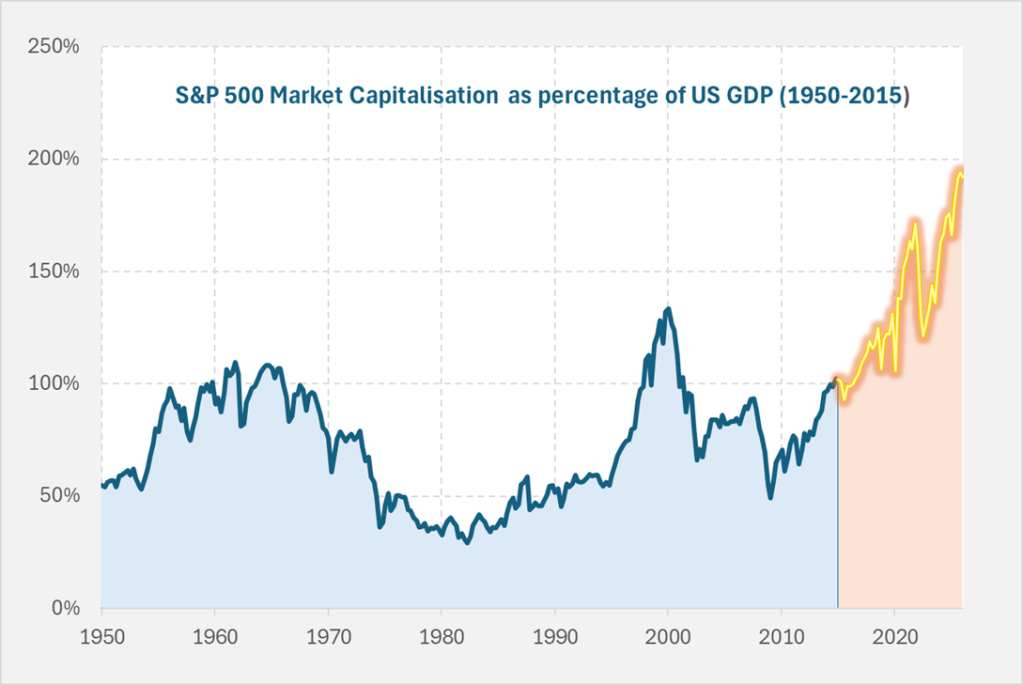

The US stock market has become enormous relative to the size of the economy. Below we show the value of US equities as a share of overall GDP. It is double what it was a decade ago, and far higher than we saw in the dot-com bubble of 2000.

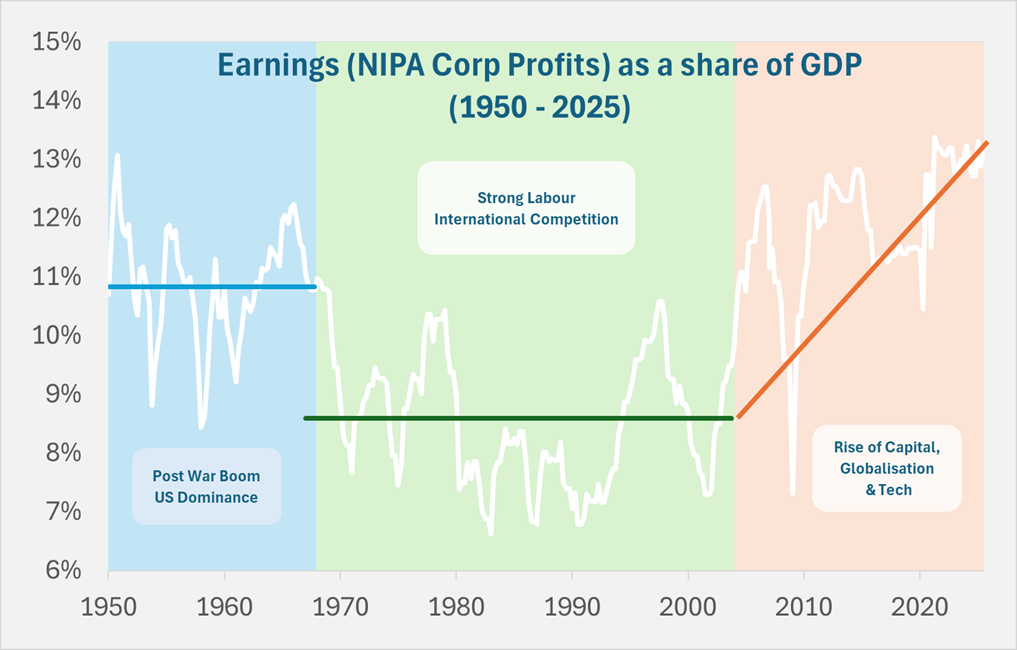

The reason this chart looks more extreme than the simple PE chart is that underlying earnings as a share of GDP has already reached unprecedented levels over the past twenty years. This rise in corporate profits from around 8.5% to 13% of GDP has seen wages stagnate, widening economic inequality, and a political backdrop marked by discontent and populist movements such as MAGA.

Current valuations show the same level of optimism about future earnings growth as in 2000 dot-com bubble, except today’s level of earnings are far higher. It is this combination that is so extreme.

What would this earnings share need to be over the next decade for your stock market investment to simply keep pace with GDP growth? The chart below shows

The projections are stark.

Current valuations assume future jumps in profitability that dwarf anything ever seen. Can AI really deliver a surge in corporate profits far beyond the gains achieved in the last waves of globalisation or past technological booms?

This series will continue on substack and examines the extraordinary claims behind these extraordinary times.

I am confused by the calm coverage of the recent radical shift in economic policy – described by the BBC as “bid to boost growth”. This type of reporting does not make clear whether we are talking short-term growth or long-term potential, and how these policies impact each of them in very different ways. From conversations with friends, much of the analysis does not investigate this and ultimately reveal just how dangerous and radical this new set of policies is.

Potential Output – what is it?

Truss has justified her policy changes economically citing improvements in the UK’s long-term growth potential i.e. increasing potential output

Potential output is the starting point for thinking about how much the country can produce ie it is the maximum sustainable level of output.

If we are below, then this is called a negative output gap and we see things like unemployment rates being high and inflation likely falling.

The OBR does a great job on this and their website is very clear

Potential Output – how can we improve it?

Everyone wants to improve potential output and there is a clear left vs right divide on how best to achieve it.

Truss is firmly in the right-wing supply-side movement of “trickle-down” i.e. give tax breaks to rich people and everyone will be better off because somehow this leads to greater potential output. Reagan was the most prominent exponent of this view but we are still waiting for any evidence that it works.

Potential Output – will it work?

I think best to simply summarise that there is no evidence that cutting taxes has any positive effect on potential output. OK – so if Trussonomics does not improve potential output, what does it do?

It does a LOT

The most obvious and direct impact is of course on inequality. She is delivering a massive cash handout to rich people. The richer you are the more you get.

The part that is getting less attention is the impact on

Fiscal vs interest rate policy mix

Debt sustainability

Fiscal vs interest rate policy mix

This policy choice has been perhaps at the heart of the political battle of the past decades and is commonly misunderstood. This is a shame as a simple quadrant model does a good job of providing a framework to compare the options clearly. (Fiscal policy is the mix of tax and spending with high spending/low tax being loose fiscal policy)

Tight fiscal -tight monetary When you are committed to fighting inflation above other policy goals. For example, the 1980s or commonly after an economic crisis when trying to rebuild confidence in the currency and debt. If used inappropriately looking at the 1930s Great Depression.

Tight fiscal – loose monetary This is the Cameron years. There is of course a debate over how tight fiscal policy should have been and on how the mix of tax and spending was managed. But it is a consistent policy mix

Loose fiscal – loose monetary This was at its maximum during the pandemic i.e. for a short term huge negative shock. If used long term it just leads to economic catastrophe.

Where are we now?

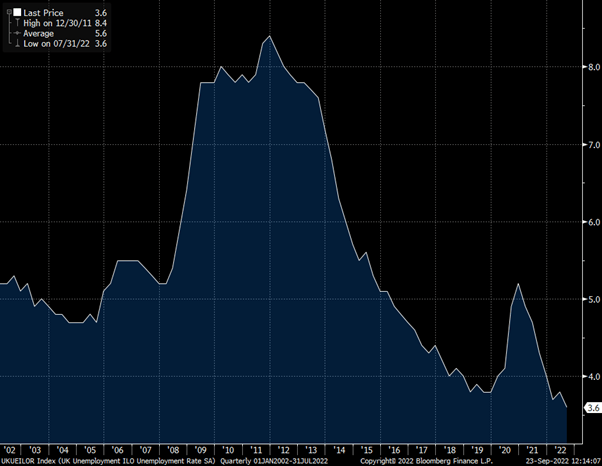

We are currently in the loose/loose box. Taking the unemployment rate as a simple measure of the output gap, you can see from the chart below we are at record lows. This is also clear to anyone trying to hire at the moment and all the reports of staff shortages. Which makes it odd that Truss talks about “boosting growth” as there is no prospect of lower unemployment from here.

UK Unemployment at record lows

The other factor that makes going for growth an odd policy goal is that inflation is high and rising. This does not have an easy solution and economic pain is unavoidable. Trying to avoid it, leads to even greater pain later.

UK Inflation at 30-year highs

What happens next?

The Bank of England will be forced to raise interest rates by huge amounts. At the start of this year the market expected interest rates to stay at around 1% though 2022 and 2023. Now the market expects rates to be 4% by the end of this year and 5.5% by the end of next year- with rate expectations for next year shifting 3% since the start of August.

What does this mean for people?

Well rich people have had a large tax cut and will be fine – I know you are all relieved to hear this.

Anyone on a regular income has had a small tax cut but this will be dwarfed by the rise in the mortgage payments coming soon.

What does it mean for the economy?

I predict a very bumpy path and hard landing for the economy but difficult to say when. The policy mix of vast fiscal expansion at a time of low unemployment and high inflation to be offset by rapid interest rate rises is a chaotic mix. I think the economy will stay strong and then crash hard.

Debt sustainability

This is getting some attention but is being dismissed by Truss. The fact that they did not let the OBR produce a forecast tells us a lot about how they have contempt for this constraint on policy. An Office of Budget Responsibility is not what the Chancellor wants to hear from!

But the bond market still exists, and long-term government borrowing is getting hammered. 30-year Gilt yields have risen from under 1% at the start of the year to 4% as I write this.

The tax cuts and extra spending increases the budget deficit. The rise in interest rates increased the cost of servicing the debt, further increasing the budget deficit. This can become an exponentially explosive mix with the major accelerator being a currency crisis as the value of sterling falls.

Conclusion

The Trussonomics experiment is radical and dangerous. I expect high inflation, high interest rates and a weak currency leading to economic crisis. Politically I expect her to start to blame the Bank of England as though the rise in interest rates was not a direct result of her policies. The Bank of England may be independent of the government, but they are not independent of economic reality.

Truss has spoken of her disdain for “abacus economics” and she does not believe things need to add up. I think economic reality exists and her magical money tree fantasy will fail.

I read an interesting article recently on Keanu Reeves acting style. Apparently in the world of acting, his style is to present himself as a blank canvas, upon which viewers can project themselves. It helps explain why I love so many of his movies (Matrix, Point Break, John Wick, Bill & Ted), but struggle to understand why, as he doesn’t appear to be a very good actor.

This style of acting certainly makes sense in the context of watching a film, we gain particular pleasure from being able to imagine ourselves as a participant in the drama. Similarly, I have also read that men watching sport are essentially fantasizing that they are actually playing themselves.

Keanu’s aim is not to overwhelm, his voice and facial expressions are muted, the personality left somewhat undefined and given this lack of concrete character, we can overwrite with our own feelings. Although I’m less of a fan, it helps explain why Tom Cruise is such a successful leading man.

This concept does not just apply to sports and movies, it occurs to me to this has wider applications:

Extension to business

An area where I find I’m mindful of this issue is when I conduct an interview at work.

If I run an informal, unstructured interview then often my impression of a candidate will relate closely to my mood. If I am highly positive and energetic, then we are likely to have an energetic conversation and I will come out thinking this person has those qualities. I tend to think well of people and so am in danger of projecting the qualities I like onto them.

Over time, I have built a more structured interview and hiring process, with a prepared common list of questions and involving independent interviewers. This helps to highlight a candidate’s strengths and weaknesses in a more objective manner.

Extension to politics

The effect in politics is also interesting, perhaps increasingly so.

The marketing of politicians has evolved over the decades. It used to be that politicians had a set of views, often described in speeches and laid out in a manifesto. Later it seems clear that to win an election you do not need to have coherent views and that the overall spin and marketing is what matters. Now, it appears that elections have moved to another level. Politicians are even more electable if their views are actively incoherent. A politician is no longer required to be a well-rounded person with specific policies and characteristics which can be evaluated – it is more important to be an avatar for the emotions of their support base.

The outstanding recent example of this is of course Trump. But it also helps explain the behaviour of the leading Brexiteers, such as Boris Johnson. A lack of coherent viewpoints is not a flaw, it is the essence of their appeal. They are liked because of their incoherence, not in spite of it. By making rambling, nonsensical speeches without the need to engage with any aspect of reality, they create a perfect blank upon which the emotions of their supporters can be projected. You do not need to look for the inconsistencies and incompatibilities within their support base, they are sure to exist. What’s more important is the common emotional need they all share, and wish to express.

This also means that whatever you think of Trump or Boris personally, they are not the real problem.

Without them, another avatar would be found to take their place. Boris will only remain the darling of the Telegraph as long as he continues talking gobbledygook in a manner they find amusing. He knows that if he gave a serious speech acknowledging the trade-offs involved in Brexit, they would find another to take his place, so he happily makes speeches which he must know are full of lies and nonsense. It is very possible that Trump does not understand any of this or that he is not in control of his movement, or even his own identity. His candidate lost the recent Alabama primary to a candidate promoted as backed by the @realDonaldTrump. Steve Bannon told a rally “a vote for Judge Roy Moore is a vote for Donald J Trump”, while Trump himself was campaigning for Sen. Strange!

The movement existed before Trump and is merely using him as its current symbol. They are in a symbiotic relationship of mutual support, and have created a powerful and dangerous, political force.

This is a term commonly used – but I struggle to understand what people mean by it.

Types of probabilistic events?

In Taleb’s book of the same name, “Black Swan” appears to be used in a variety of ways:

For a well-defined outcome with a low probability

for example: selling lottery tickets or buying CDOs in 2006/7.

(perhaps the people buying such CDOs did not understand that they were selling lottery tickets but they should have!)

For general uncertainty We all know it is possible to have a currency crisis in the UK in the next 5 years but it is not very sensible to put a single number on it. This is concept of “uncertainty” from Knight and Keynes and many macro issues fit into this category. A frequentist approach to probability works for rolling dice but often not for rare events.

For “fat tail” events

Extreme events occur in reality more commonly than a normal distribution would suggest.

For when the distribution is just unknown It is possible that it will be known at a later stage, but currently there is insufficient information.

For an unknown, possible outcome

This seems to be the new, popular meaning.

Numbers 1 through 4 are well-known and have perfectly good ways to describe them. I think that only number 5 really makes sense as a potential separate meaning for “Black Swan”.

Does number 5 actually exist?

This is also the meaning I have most problem with as I struggle to find real-world examples of it. There are many examples where people did not consider the possibility of a given outcome, but at the same time you can find many people who did and even had decent reasons to expect it to happen. At the individual level it makes some sense as being imaginative can be hard work! However, if some people are not surprised at the occurrence, then how can it be something which “is not even imagined as a possibility prior to its occurrence” unless as you say it is entirely subjective and individual.

It may have been unimaginable to Cheney that the Iraqi people did not embrace US troops as liberators in 2003. Does that mean it was a Black Swan as it was not conceived possible and was clearly important? Or does it just mean Cheney was wrong?

Common usage

Let’s consider what many see as the great Black Swan of 2008:

This is what I think people mean:

· 2008 was a massive drop in markets

· A great deal of common practice in managing risk was terrible

· They didn’t see it coming because it was unforeseeable

Therefore

· I should not feel bad about not predicting it

· Black Swans are very rare, so we should not expect it to happen again

· We should carry on pretty much as before

Why it annoys me

This version of events is just an excuse for being wrong, for not learning from it or changing behavior. It should be obvious that I find the term annoying in this way of excusing poor decision making and avoiding responsibility.

Alan Greenspan indeed said that the financial crisis was “unforeseeable”.

On Epistemology

Another confusion I had about the theory of the “Black swan” laid out in the book, is the way it sits at odds with the philosophy of science and specifically Popper. Popper, in fact, gets no mention in Taleb’s book, even though Popper’s key concept of falsifiability has long been linked and explained via the original example of black swans.

Quick aside on jargon

A conjecture – is an unproven proposition which appears correct

A hypothesis – is a testable statement

To illustrate Popper’s concept:

If your hypothesis is that all swans are white.

It would be disproved if you find a black swan.

Given its falsifiability, this is compatible with scientific enquiry

It is clear in this example, to be testable, you have to have considered what events would falsify it.

If we now put Taleb into similar language:

Taleb

a Black Swan is an unimagined event for certain people which disproves their conjecture

Popper a Black Swan is a defined event which would falsify a hypothesis

Written this way, I think it show the two meanings are incompatible. Popper’s version makes sense and is useful. It is therefore such a shame that Taleb’s popularisation of the term “Black Swan” has taken something important and meaningful and turned it into nonsense.